Operators and developers of commercial real estate (CRE) who raise capital directly may be missing a valuable opportunity. Engaging an investment banker and broker-dealer may be able to simplify and expedite the process, regardless of the financing tranche needed, by introducing you to multiple investors through a private placement (PP).

This article explains private securities and private placements. Targeted to owners and developers of commercial real estate, it covers:

- How private placements apply when seeking debt and/or equity,

- What types of investors are attracted, and

- How PPs work for various situations.

But first, let’s review some basics.

What is a Security?

A security is a form of financial asset held by an investor issued by legal entities (the issuer) to raise capital from investors expecting to profit from the exchange. Securities include proofs of ownership (equity) or indebtedness (loans, such as promissory notes) that are assigned a monetary value. For the security holder, it represents an investment with rights of ownership or priority in the event of liquidation.

Loans are issuer liabilities with interest payments and note principal repayment obligations. U.S. securities laws broadly include promissory notes) under the definition with certain exemptions. *

In general, it’s safe to assume that, if a business is borrowing from non-bank third parties, the activity falls under U.S. securities laws.

Equity represents ownership stakes in a company with owners generally participating in the profits. Preferred equity holders have a higher claim on profits than common equity holders and, typically, have no voting rights.

What are Private Placements?

Private placements are discrete offerings of securities, where, traditionally, the information provided by issuers to investors is not publicly available through advertisements or news stories. These offerings are not publicly registered with the U.S. Securities and Exchange Commission (the SEC) before being made available to investors, making them a significantly less expensive and easier process than issuing a public security.

U.S. Securities Laws Relating to Private Placements

If a CRE owner/developer seeks financing through a private placement, an investment bank should help observe certain U.S. securities regulations. PPs must follow a “manner of offering” authorized by the Securities Act of 1933 and with issuance guidelines specified in SEC regulations, primarily Regulation D. Importantly, these laws and regulations specify the manner of offering to investors, not the type of security being sold.

Private placements can involve virtually any type of Security, including debt or equity interests (e.g., common stock, preferred stock or membership interests in an LLC. No matter where in the capital stack the financing is needed, a private placement can be used.

Regulation D (“Reg D”), established by the SEC in the 1980’s, defines more specifically a manner of privately offering securities. Most companies do so by following one of the rules within Reg D Rule 506(b) allows companies to issue an unlimited amount of securities so long as no more than 35 non-accredited investors participate in the offering. Rule 506(c), approved by the SEC in 2013, permits the issuer to make a “general solicitation” (i.e., advertising) for Reg D offerings, but only accredited investors may purchase the securities.

No matter the manner in which they are offered, these private placements can be sold solely directly or via a registered broker-dealer (“b/d”).

Traditional CRE intermediaries such as investment brokers and debt/equity brokers cannot promote a Reg D offering unless their firm is also a registered B/D. If they use an unregistered “finder” to receive transaction-based compensation, they may face significant legal and regulatory implications, and the issuer may need to provide investors with the right to rescind their investments.

Who Invest in Commercial Real Estate?

For CRE companies, accredited investors can include high-net-worth individuals, family offices, self-directed IRAs, trusts/estates, institutions, alternative investment managers, offshore investors, larger private investment groups, and EB-5 investors.

Each has a varying risk/return profile, security and capital tranche preferences, asset classification (e.g., core, core+), and investment holding period goals.

An investment bank with a broad investor network can introduce issuers to individuals or institutions who may become ongoing investors in future financings.

Where can Private Placements Play in the Capital Stack?

Private placements can fund various organizational levels, such as the operating company, project, portfolio, or investment fund. Perhaps the sponsor needs project finance to renovate an old shopping mall. If they’ve already found debt financiers, they may wish to issue preferred equity to round out the capital raise. Or, rather than project financing, they may have decided to acquire a portfolio of assets and require financing` this at the corporate level.

When it comes to how the funds may be used, they are very versatile. A PP can fund acquisitions, new development, recapitalizations, real estate roll-ups, and/or platform growth. The classification (e.g., core or opportunistic) is equally immaterial.

Why Draw Upon an Investment Bank and Broker-Dealer?

In Carofin’s experience, many sponsors already have identified financiers. However, for those who don’t, employing these specialists offers several advantages:

- Expansive Investor Network: A broker-dealer should be able to introduce the project to thousands of potential investors, extending far beyond the sponsor’s direct network.

- Reduced Demands on Time: Raising capital is the broker-dealer’s full-time job, freeing sponsors to focus on their core business.

- Deal-Structuring Expertise: Understanding investor preferences and issuer cash flows are critical components when crafting a security that fits the issuer’s needs and attracts investors.

- Satisfying Compliance Requirements: Investment banks handle regulatory requirements, from producing compliant sales materials, to drafting documentation, maintaining records for FINRA, and generating SEC filings.

Key Considerations When Selecting a Banking Partner

In some investment banks, the bankers do it all: they source clients, conduct due diligence, structure the security, sell it, and support the investors with ongoing investment updates.

For many, this is not the optimal structure. The best investment bank/broker-dealer firms have separate investment banking teams to structure and price deals, conduct comprehensive due diligence, and keep investors informed post-closing.

Their syndication teams of registered reps will know the investment criteria, risk/return profiles, motivations, and capital availability of each of their registered accredited investors. A b/d that aligns dedicated registered reps with each investor is likely to close offerings more efficiently than the alternative.

Experienced firms can also draw upon intermediaries representing high-net-worth investors, including RIAs, wealth managers, financial advisors, and other broker-dealers.

Multi-dimensional Offering Strategy: One Size Does Not Fit All

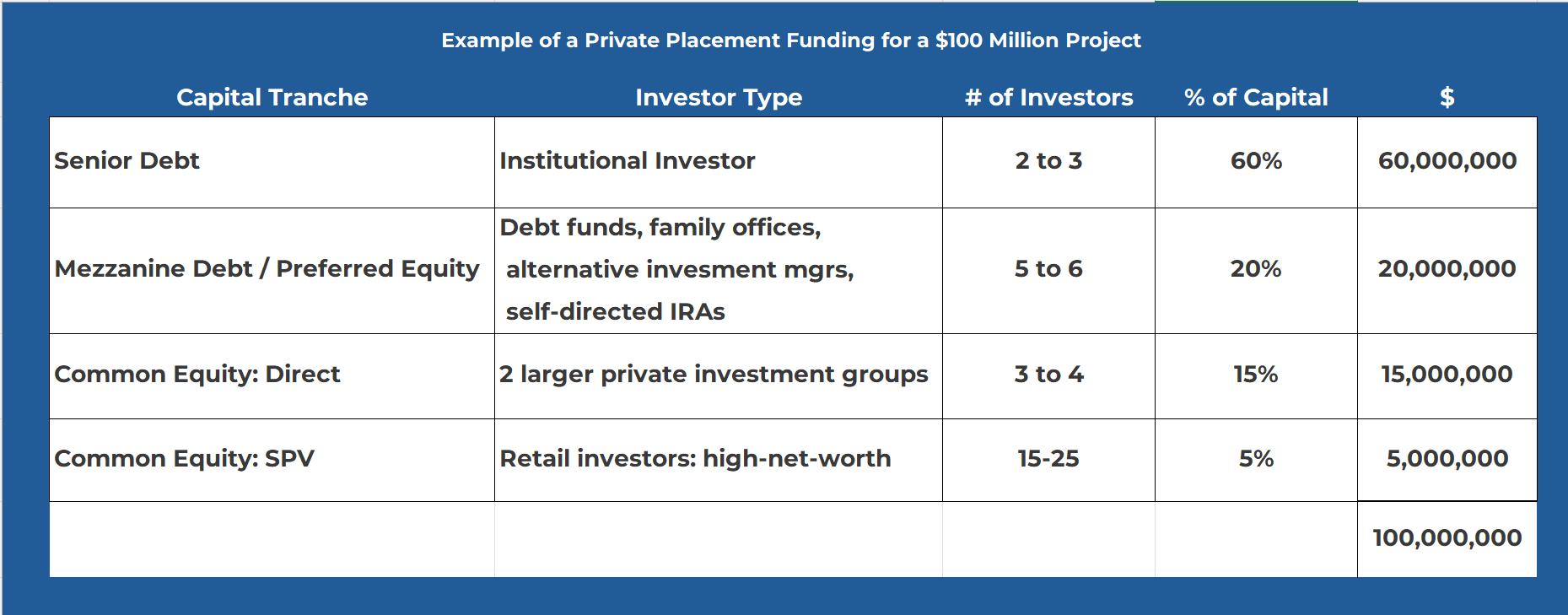

Typically, a sponsor will raise capital from diverse sources through different tranches of the capital stack – senior debt, mezzanine debt, preferred equity, and common equity. For instance, a Houston developer wants to raise $100 million for a medical office building. They likely can draw from their sources to find the senior debt. However, when it comes to sub-debt and equity to fill the raise, they can use an investment bank to raise the capital simultaneously across tranches, as the type and number of investors can vary greatly.

Bottom Line

Raising capital for CRE projects through private placements, facilitated by an investment bank/broker-dealer combination, can enhance the speed and efficiency of the process by leveraging multiple investor types and extensive networks. This combination offers broad investor networks, deal-structuring expertise, and the added assurance of regulatory compliance.

We invite you to go to our website to learn more about how we serve our issuers.

* The U.S. courts have exempted certain categories of lending arrangements from the definition of securities, even though they may still be subject to banking regulations, including consumer-finance notes, home mortgages, and notes related to commercial bank activities.