The Unites States Craft Distillers market has been growing more rapidly than the equivalents in beer and wine. And the pace is likely to accelerate. This article examines the principal drivers of the market’s growth and its prospects.

DEFINITION

According to the Spruce Eats, distilled spirits are alcoholic beverages that have been “distilled from grains, fruits or other fermentable ingredients. The seven core spirits include brandy, gin, rum, tequila, whiskey, vodka and flavored liqueurs. As with beer and wine, producers ferment the contents, producing alcohol.

Corn, wheat, and rye grains produce whiskey, vodka or gin (although some vodkas are made from potatoes). Rum is created by fermenting molasses, tequila and mezcal begin with juices from the agave plant, and brandy from fruit juices.

BEVERAGE INDUSTRY STATISTICS

The beverage industry can be classified into alcoholic and non-alcoholic beverages.

While conflicting statistics abound, it appears that the 2019 North American non-alcoholic beverage market was valued at nearly $400 billion (another source indicates it was as large as $620 billion). As of July 2021, the U.S. alcoholic beverage market in 2019 was $250 billion.

There are three broad categories within the beverage alcohol market: beer and malt-based products, wine, and spirits. In 2020, beer and malt-based products represented 44% of the market, distilled spirits 39.1% and wine sales comprised 16.9%. The Distilled Spirits Council of the United States (DISCUS) reported that 2020 represented the 11th consecutive year that spirits sales continued to gain market share from both beer and wine.

DISTILLED SPIRITS

There are 5,000 brands of distilled spirits on the market, with hundreds of new entrants arriving each year.

Vodka followed by whiskey are the two most popular categories. Agave-derived drinks (tequila and mezcal) are in third position, recently supplanting rum.

Four segments make up the market: Non-Premium, Premium, Super-Premium and Ultra-Premium.

Grandview Research reports that, over the past few years, the high-end alcohol segment has been outpacing the growth of the overall segment, growing worldwide consumption of alcohol. Much of this growth is attributable to craft distillers.

Distribution channels also divide the market: off-trade and on-trade. The on-trade segment split into restaurants, bars, clubs, cafes, and hotels. Off-trade includes all retail outlets (think hypermarkets, supermarkets, convenience stores, mini markets, kiosks, wine, and spirits shops, etc.

CRAFT DISTILLED SPIRITS

What sets a craft spirits distiller apart from the larger universe? In their Annual Craft Spirits Economic Briefing from November 2020 (from which much of the following draws), the American Craft Spirits Association industry participants generally agree that a licensed craft distillery:

- Must distill and bottle the products on-site,

- May not produce more than 750,000 proof gallons (or 394,317 9L cases) per year,

- A large supplier may not openly controlled it, and

- Have no proven violation of the American Craft Spirits Association’s (ACSA) Code of Ethics.

A proof gallon is a gallon of spirit with an alcohol by volume (ABV) of 50% or more.

As of August 2020, there were 2,265 active craft distilled spirits plants (out of a total distillery industry of 3,606, which includes non-craft DSPs.

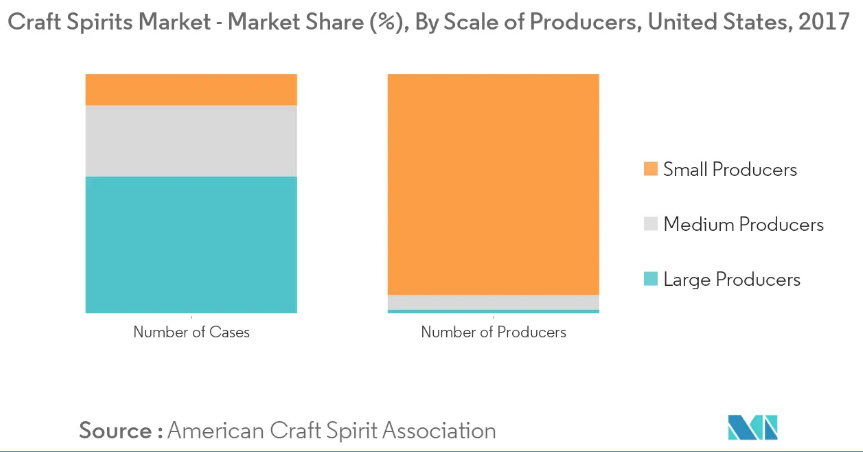

Large craft distilleries generally produce between 100,000 and 750,000 cases annually and control much of the market. Only 1.6% of distillers in the U.S produces 57.2% of the cases sold. Smaller distillers (producing 10,000 or fewer proof gallons) sell 11.7% of the cases. Around 60% of craft distillers sell fewer than 2,500 cases per year and 70% employ 10 or fewer employees.

GROWTH IN THE CRAFT SPIRITS INDUSTRY

By practically every measure, craft distilling has grown at a rapid rate.

- Between 2011 and 2017, the number of spirits distilleries increased by roughly 35% annually

- Craft spirits market sales have grown 19%/year since 2015.

- Between 2014 and 2019, craft distillers’ volume has nearly tripled.

- From 2018 to 2019, the sales volume of the U.S. domestic market grew 24% (measured in 9L cases), well above its CAGR between 2011 and 2017.

- The equivalent in value grew from $1.8 billion to $6.1 billion, an annual growth rate of 27.1%.

- More recently, the number of active craft distillers in the U.S. grew by 10.7% to 2,265 between 2019 and August 2020.

Market Share: Craft spirits are growing their share of the spirits market. In 2014, they accounted for only 1.8% of the spirits market in volume and 2.3% in value. By 2019, however, they had reached 4.6% in volume and 6.9% in value in 2019. Optimism abounds among retailers and wholesalers about the continued growth of craft spirits. They believe that this market “can perform as well or better than craft beer… 60% of wholesalers think that craft spirits will become more relevant to the liquor industry than craft beer is to the beer industry.”

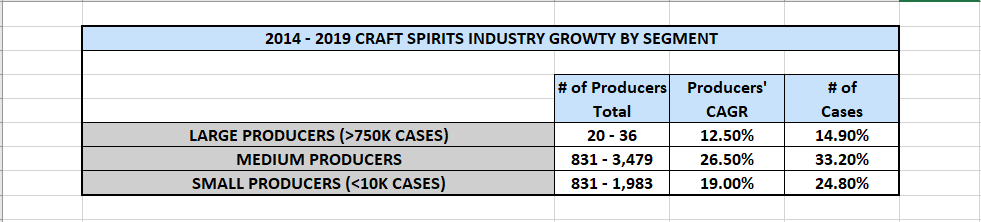

Growth by Segment: Medium-sized craft producers have grown at the fastest clip between 2014 and 2019 when measured both by number of producers and volume of cases produced.

Producer Comparison:

Source:Mordor Intelligence

Industry Employment: Furthermore, employment has been rising. The industry employed 30,000 in 2019, up 5,000 from the previous year.

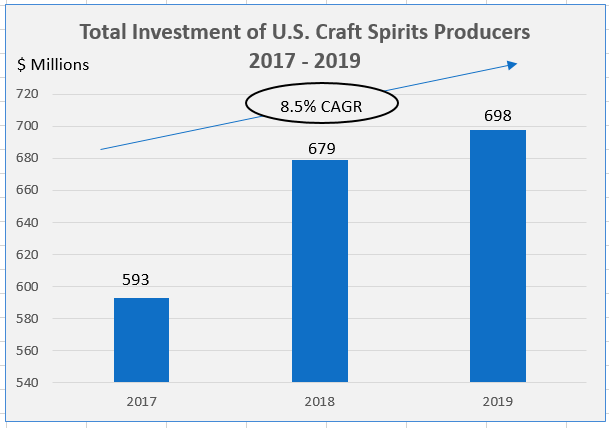

Investment: Prospects continue to look good for the industry. Consequently, U.S. craft spirits producers’ investment has been on the rise. In 2019, invested capital rose by $19M over 2018 to $698 million.

Source: Craft Spirits Data Project

Market Consolidation: Furthermore, two trends — rising demand and larger players seeking to expand their markets and product suite — should accelerate industry consolidation. Between 2014 and 2017 alone, there were more than 25 spirits M&A transactions.

GROWTH DRIVERS IN CRAFT SPIRITS

Numerous factors are contributing to the rise of the craft spirits industry.

Legislation:

- One of the most significant contributions was the enactment of the Craft Beverage Modernization and Tax Reform Act. Passed in 2017 and enacted over 2018 and 2019, it gave tax relief to brewers, winemakers, distillers, and importers of alcoholic beverages. Had it not passed, tax rates on distillers would have reverted to previous levels – a 400% increase. As previously noted, this has generated a wave of investment by distillers in new facilities and equipment. The act equalized the federal excise tax (FET) on spirits, beer and wine on the first 100,000 gallons for all producers and resulted in a significant reduction of the FET for craft producers, from $13.50 per proof gallon to $2.70 per proof gallon.

- Tax threats were defeated in 19 states in 2018, saving the sector over a half a billion dollars.

- Additionally, two more states, Indiana and Tennessee, approved Sunday sales of liquors, and the ban in West Virginia was lifted, making a total of 43 states that have ended the Blue laws prohibiting certain activities and sales of products.

- Consumers are now allowed to sample distilled spirits in advance of a purchase in 48 states, leveling the playing field with wine tastings and contributing to the premiumization trend described below.

- Cocktails to-go: Because of the deleterious effect COVID had on restaurants (a 78% reduction in restaurant sales), 35 states and the District of Columbia have allowed restaurants and bars to sell cocktails and distilled spirits to go, to be picked-up or delivered.

Premiumization, a term used to describe the shift from non-premium and low-premium spirits to the finer, more expensive spirits, has taken root, particularly among millennials. They are moving forcefully into diverse, innovative, and authentic high-end super- and ultra-premium products. Comprising 29% of the drinking age population, they consume 32% by value of spirits. In other words, they are selecting more premium and ultra-premium products.

According to Grandview Research report from August 2020, the global premium spirit market size in value in 2020 was $135.76 billion. By 2027, projections indicated that value would soar to $235.74 billion. Note: some projections cited here were made prior to knowing the full effects of COVID-19. Where possible, the author has sought to cite what appear to be tempered projections.

“From 2015-2016, premium brands grew more than twice as much as non-premium brands in almost every category,” reported Park Street. Total U.S. premium product growth in the U.S. was 9%. But between 2016 and 2021, industry insiders projected premium brands’ growth of their market share at 23.6% versus only 2.9% for non-premium products.

Over the last several years, premium and ultra-premium tequila have been among the fastest growing spirits, contributing to the premiumization trend (Source: Joseph Micallef’s article, The Future of Ultra-Premium Tequila in the January 17, 2019 issue of Forbes Magazine). This is even though prices for tequila now range from $50 to over $1,000 per bottle.

Some tequila producers value certain processes, but they add costs. Using 100% blue agave (increasing the quality of the agave), for instance, drives up producers’ and consumers’ cost. Only a handful of producers, unwilling to sacrifice taste for efficiency, use certain production methods. These include employing a tahona to crush the agave instead of switching to high-speed roll crushers. Utilizing small capacity brick ovens (hornos) to cook agave slows the process and, thereby, increases the cost. Producers are even experimenting with the aging process. Some are switching from the easily obtained ex-bourbon barrels to other barrel types, such as sherry, port or cognac. These cost more but attract consumers looking for unique tastes. Finally, producers are experimenting with the time the tequila rests in barrels. All these contribute to the rising price of premium and ultra-premium tequilas.

Reporting the ninth straight year of record spirits sales in 2019, the Chief Spirits Council Chief Economist David Ozgo …

Pointed to the strongest growth in high-end premium and super premium products across most categories. The revenue for those price points increased 8.9 percent and 10.5 percent, respectively, and by 8.0 percent and 7.5 percent for volume.

Perhaps driven by millennials as well, many consumers are seeking clarity and sustainable manufacturing practices. This also creates the opportunity for firms to offer products at premium price points. A related trend is the “Better-for-you movement,” which has buoyed vodka sales in particular – driven by the diet, sugar-free vodkas and naturally-flavored brands.

Cocktail Culture: A recent phenomenon also has taken hold – a “cocktail culture,” replete with innovative cocktails. Malt beverages, while still king, are losing market share to premium spirits. But even the beer market is adapting. While craft beer represents only 12% of the larger beer market, larger brands are developing products to capitalize on the trend.

Drinking at Home: More people are mixing drinks at home, and ready-to-drink (RTD) cocktails are coming on strong to meet the demand. In 2020, RTDs posted a 26.4% growth across the globe, the largest gain in any alcoholic beverage category. Predictions for 2021 indicate an even larger gain of 26.6% volume sales increase.

e-commerce: Brands are using social media to drive off-premise sales, and e-commerce cocktail clubs are becoming more widespread, just as were wine clubs that preceded them. In 2019, worldwide online grocery alcoholic beverage sales experienced a 115% growth since 2017. Wine led at $145 million, beer at $115 million, and spirits at $35 million.

Margarita cocktails with different flavors

WHICH SPIRITS ARE LEADING THE GROWTH?

Four spirits are gaining market share: whiskey, tequila, brandy and cognac are gaining momentum, and the industry is responding with flavored liquors and nonconventional and/or experimental processes.

In 2021, the Margarita is reportedly the most popular cocktail in the world, according to research conducted for World Cocktail Day. Tequila sales grew 9.6% in 2020, overtaking rum as the third-largest spirits category in the U.S. This data is supported by the Distilled Spirits Council, noting that total volumes in tequila consumption have grown 209% between 2002 and 2020.

According to a Grandview Research report from August 2020, consumers have been embracing tequila as never before. Gone are the days of the “party shot.” Cocktails like Margaritas and Tequila Sunrises are becoming more popular. Furthermore, high-end brandy or whiskey products are well established, whereas premium options for tequila are relatively new. Consequently, this trend will encourage producers to invest in premium tequilas.

Growth in the premium spirits segment compared to the non-premium segments was projected to be 23.6% vs. 2.9% CAGR respectively between 2016 and 2021. Within the global premium market, Grandview Research projected that the tequila segment was expected to register the fastest revenue CAGR of 11.6% from 2020 to 2027.

EFFECTS OF COVID-19

Despite the dramatic effect that the pandemic has had in on-premise sales, consumption of alcohol in the Unites States increased by 2% last year, “its biggest year-over-year increase since 2002.”

As widely reported, COVID has affected business mechanics, from supply chains to ecommerce adoption. On-premise sales of distilled products in bars and restaurants plunged during the lockdowns. According to one source, COVID-19 led to a 78% reduction in revenues from restaurant sales.

According to the Distilled Spirits Council and the American Distilling Institute in August 2020, almost 41% of craft distillers derive > 50% of their revenues from on-site tasting rooms, which were decimated in the pandemic. Approximately 40% of craft distillers lost approximately 25% or more of their on-site sales. Over 15% said that they closed their tasting rooms. The combined loses in wholesale (for distribution to restaurants) and tasting room sales represented a 41% drop in craft business.

However, the pandemic also accelerated growth in off-premise sales by brands using social media platforms. So, too, did it spur the growth of distilled spirits clubs on-line and liquor store sales.

Despite challenges in specific sales channels, total spirits sales rose 4.6% last year, the biggest increase since 1990. The Craft Spirits Data Project noted that the majority of craft producers experienced a double-digit decrease in sales in the first half of 2020, as compared to a 27.1% increase in 2019. Agave-based spirits jumped 15.9% last year, placing tequila in third place behind vodka and whiskey. The clearest winner in category growth was the RTD. It registered a rise of seismic proportions: 63%, boding well for continued acceptance.

Change is in the wind. COVID-19 is still limiting sales in the U.S. However, two populous states, New York and Texas, have lifted COVID restrictions in June 2021, re-opening on-premise sales. More will most likely follow in short order. According to the IWSJ Drinks Market Analysis, alcohol sales are projected to grow by nearly 3% globally and nearly 4% in the U.S. in 2021.

INDUSTRY PROSPECTS

According to the IWSR Drinks Market Analysis, total alcohol consumption is expected to return to pre-COVID levels by 2023. U.S. sales are projected to increase at a CAGR of 5.02% from 2021-2026, and the premium spirits market is expected to grow at a CAGR of 10.3% between 2020 to 2027.

Because of COVID lockdowns, premium brands have embraced ecommerce and revenues stemming from the off-trade distribution channel. Industry experts expect this distribution channelto grow the fastest. The industry has nimbly adapted to ecommerce and RTD sales, among other trends. Its growth is not likely to abate.

The craft spirits market is also poised for growth. Contributing factors include a focus on quality products. Strong grassroots marketing abilities and a broader portfolio of flavors and enhanced production capacity is also aiding. As a result, larger firms are likely to accelerate acquisitions to close gaps in their portfolios.

Prospects for continued growth in the craft spirits markets remain bright.