A young company approaches you. “Invest in us,” they say, “and your shares will be worth millions.” What are they offering, and does the structure make the most sense for you and the company?

For the past quarter-century, we’ve been approached by companies – some little more than concepts – that showed promise. Many satisfied the first principles described in Carofin’s White Paper, Primary Investment Considerations. There’s a fundamental societal need that exists now, they’ve correctly identified the challenges, and their solution is unique. At least on paper, they should be profitable.

You’re on the right track. Maybe it’s worth digging deeper. Is investing in this company a smart move? Let’s look more closely.

Example:

A young, SaaS-based medical technology firm outside Boston (we’ll call it “MedSolv4U”) was seeking to raise $2,000,000. Why? It needed to invest in order to keep its product competitive. It also needed to hire a sales team.

A Promissory Note?

The question was what to offer investors. One firm advised it to structure a promissory note. Remember, a note generally requires a company to pay interest. Often, it also obliges the issuer to return some amount of principal monthly to the lenders.

However, the company’s revenues were erratic. Although its pipeline was growing (a promising sign), its revenues weren’t steady. Think of an apartment complex with constant rent rolls, or a more established company with long-term customers and contracts. So, when building the company was most important, a note would increase its fixed costs and might put the company in a bind.

Shares in the Company?

To avoid that mistake, MedSolv4U decided to sell a stake in the company. In this way, there would be no current drain on the company’s cash flows. In return, the original owners would be foregoing some of the future value in the company.

Again, remembering equity fundamentals, an investor wants as high a stake as possible in a company. Two hundred thousand shares of a company whose value is $10mm represent a larger stake than the same number of shares in a company worth $100mm. Convincing an investor to accept the company’s estimated value, particularly at this early growth / late venture

stage, is difficult at best.

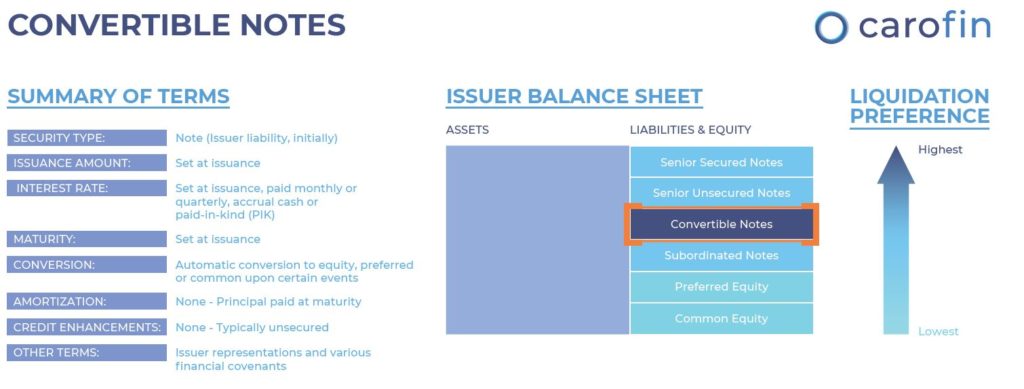

Convertible Note

The solution? One experienced private investor recommended a hybrid security – a convertible note — because of its flexibility. First, a convertible note does not amortize. Furthermore, although it bears an interest rate, the coupon either can be paid currently OR can accrue. Choosing the latter means that a convertible note does not add a current demand on the company’s revenues. But it also offers the investor the upside potential of an equity investment.

The illustration below will help define how convertible notes work. They are loans, with defined maturities, interest rates, no amortization and pre-determined conversion circumstances. The rate can accrue until such time as either the note matures, the company is bought, goes public, or a pre-defined event occurs that triggers the conversion into equity. At maturity or conversion (if the interest rate has been accruing), the investor realizes a return. That can be in the form of principal plus accrued interest or shares that have increased in value between the time of investment and a liquidity event.

In this case, the company in our example took the investor’s recommendation. While still premature to say, the company continues to grow, and the Route 128 corridor around Boston is likely to produce a few more millionaires in the next several years.

Understanding how suitable a security is for the company’s circumstances, the way the security works, and whether it fits your alternative investment goals, is all part of an investor’s due diligence process. It’s your money, and you should make sure that the investment is right for you.

The MedSolv4U case is a good example of how important a security structure is to each investment. However, it is not the only factor that can affect its success. If MedSolv4U failed to meet its objectives, or regulations affecting its business had a material adverse impact, the correct security structure alone would not guarantee returns to the investors in the company.

For a more complete discussion of different security structures that are commonly found in

private placements, please read Carofin’s Understanding Private Securities.