The traditional asset allocation model that Registered Investment Advisors (RIAs) have followed since the mid-twentieth century is undergoing a profound transformation. Alternative assets are edging closer to “core” investments, including within this broad category, private placements. This shift reflects the evolving dynamics of public and private markets, the growing scale and performance of private investments, and the ways RIAs and their Financial Advisors are adapting to provide additional value-add services while meeting investors’ increasing demand for these opportunities

Evolution of the Public and Private Markets

Over the past 25 years, changes in both public markets and client portfolio strategies have dramatically reshaped the landscape for U.S. RIAs. A significant factor in this evolution has been the regulatory environment. After the tech bubble burst in 2001 and the subsequent Sarbanes-Oxley Act of 2002, regulatory requirements and compliance costs have escalated, making the path to public listing less appealing. Consequently, many emerging companies are opting to stay private longer.

However, increased regulation is not the only factor driving this trend. The diversification benefits and enhanced returns offered by private markets have compelled Investment Advisors and RIAs to reassess the conventional 60/40 portfolio model. Among the most notable trends are:

- Since 2009, companies have consistently raised more capital in private markets than in public markets.1

- The number of publicly listed companies on U.S. exchanges has sharply declined, from nearly 8,000 in 1996 to approximately 3700 in 2023, significantly narrowing investment options.2

- With fewer initial public offerings, publicly listed companies are aging, resulting in lower returns due to later-stage investments.

- Net investment returns in private equity (PE) have consistently outperformed the S&P 500 since 2001, with only one exception, often by substantial margins.3

- Similarly, private credit has outperformed public leveraged loans, its public market equivalent, for over 2 decades. 3

Technological advances have further diminished the allure of public markets for RIA clients. The rise of algorithmic trading not only has eroded the potential for capturing market inefficiencies but also exacerbated systemic risk and market volatility, challenging the effectiveness of traditional public market investments.

Alternative Investments: A Diverse Landscape

The world of alternative investments is remarkably diverse, encompassing a wide array of asset classes. From real estate, commodities, and farmland to collectibles, cryptocurrencies, venture capital, private equity, and more, alternative investments offer a broader spectrum of opportunities and have a deeper bench compared to the limited selection available on the U.S. exchanges. According to the U.S. Securities and Exchange Commission, excluding direct private investments in individual companies, an investor have access to over 43,500 funds across various categories. For more information on the variety of alternative investments, please see our article on What are “Alternative Investments?”

This broad array allows individuals to participate in a vast range of industries and asset types (e.g., debt or equity), whether through professionally managed funds or direct investments in companies.

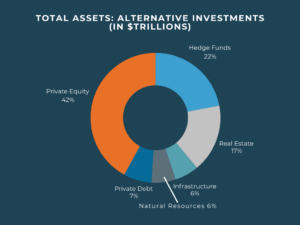

Two decades ago, the total assets invested in alternatives stood at $4.8 trillion, representing a mere 6% of global assets under management (AUM). At that time, hedge funds dominated the alternative space. However, private equity has emerged today as the leading category within alternative investments, commanding $22 trillion in AUM, or 15% of global AUM. Despite this growth, financial advisors (FA’s) report that real estate remains the most widely utilized alternative investment, with 72% of survey respondents indicating a current allocation in their clients’ portfolios.4

Two decades ago, the total assets invested in alternatives stood at $4.8 trillion, representing a mere 6% of global assets under management (AUM). At that time, hedge funds dominated the alternative space. However, private equity has emerged today as the leading category within alternative investments, commanding $22 trillion in AUM, or 15% of global AUM. Despite this growth, financial advisors (FA’s) report that real estate remains the most widely utilized alternative investment, with 72% of survey respondents indicating a current allocation in their clients’ portfolios.4

The image to the right highlights both the breadth of available strategic choices and the depth of investment within alternative investments.

Performance in the Private Markets

As the pool of public investment opportunities has dwindled, investment advisors have turned increasingly to private equity and private credit funds and, to a lesser extent, to direct private investments. The appeal of these funds lies not only in their liquidity and professional management but also in the diversification they provide. However, these benefits come with associated costs.

A typical closed-end fund, which aggregates investor capital to invest in private companies or assets, charges a management fee ranging from 1.5% to 2.0% of committed capital during the investment period, which typically spans 3-5 years. Additionally, private funds often include a carried interest fee – commonly set at 20% of investment profits – that fund managers earn after surpassing a minimum return, often around 8%.

Despite these costs, the impressive performance of private funds has justified the fees. A comprehensive analysis by Hamilton Lane, encompassing over 50,000 funds and more than $16.9 trillion in private capital, demonstrates that private funds have consistently outperformed public market benchmarks for over a decade, even after accounting for management fees and carried interest.

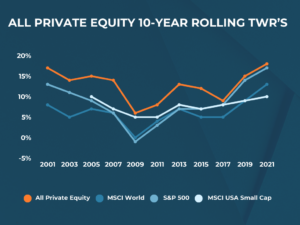

The illustration to the left compares the net-of-fees returns of private equity funds against the S&P 500 and two highly regarded global indexes, the Morgan Stanley Capital International World Index and its small-cap equivalent.

The illustration to the left compares the net-of-fees returns of private equity funds against the S&P 500 and two highly regarded global indexes, the Morgan Stanley Capital International World Index and its small-cap equivalent.

This analysis over two decades reveals that PE funds consistently outperformed other asset classes, except for a brief period in 2009 and again in late 2018 and 2019.

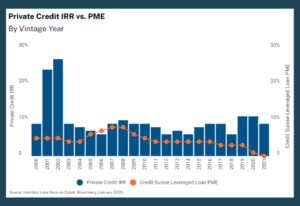

Similarly, private credit funds shown right have also demonstrated superior performance, outpacing their public market fixed-income equivalents – specifically leveraged loans – by an average of 625 basis points annually for over 20 years.

Similarly, private credit funds shown right have also demonstrated superior performance, outpacing their public market fixed-income equivalents – specifically leveraged loans – by an average of 625 basis points annually for over 20 years.

Consequently, financial advisors and investment professionals are increasingly expanding their knowledge and expertise in private alternatives, recognizing their potential to deliver enhanced returns.

RIA Adoption of Private Investments

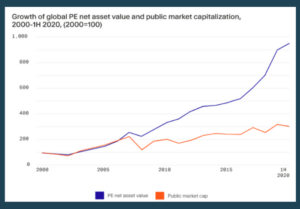

As financial advisors become increasingly knowledgeable about and comfortable with alternative investments, and as more individual investors seek to allocate assets to these opportunities, private investment adoption is steadily rising. The growth in private equity investment since the turn of the century illustrates the expanding interest in private placements, both  through funds and direct investments.

through funds and direct investments.

Between 2016 and 2021, private equity assets under management (AUM) surged, driven by a 58% increase in the number of private equity firms during this period. This growth is largely attributed to the “abundance of capital, the search for higher yields, and the globalization of the industry,” according to Forbes. Despite the challenges faced by private equity in 2023, financial advisors expect this trend toward alternative investments to persist. A 2023 survey by iCapital revealed that 95% of financial advisors planned to maintain or increase their allocations to alternatives. While institutional investors dominate the private securities market, individual investors hold an estimated 5% of alternative asset investments.5

The once-standard 60/40 allocation model – 60% equities, 40% fixed income – is evolving into a 50/30/20 model, where alternative investments comprise 20% of the portfolio. Financial advisors, constrained by public market limitations, are citing the benefits that private placements offer.

60%/40% is becoming 50%/30%/20%

Direct Private Placements

Within the broader landscape of alternative investments lies a distinct category – direct private investments. Although data on the size and scope of this market are less readily available, it is reasonable to assume that the opportunities in direct private investments far exceed those in the private fund market.

The distinction is straightforward: instead of investing in a pool of private assets, direct private placements involve investing directly in a single private company. While these investments do not offer the portfolio management services provided by fund managers, those facilitated by an investment bank and broker-dealer typically undergo rigorous background checks and due diligence. Additionally, these intermediaries may continue to monitor the performance post-investment and intervene if the investment deviates from expected outcomes.

Investors can diversify their portfolios by directly investing in multiple companies. One distinct advantage to private company investing versus private funds investing is the absence of management fees and carried interest in direct investments. As a result, the return on a direct investment aligns more closely with the actual performance of the underlying company and security; fees do not reduce investment returns. For more information on investment returns, please refer to Carofin’s guide on Alternative Investment ROIs.

Drivers of Client Demand

Retail and institutional investors are increasingly gravitating toward private placements and away from public market counterparts, driven by the pursuit of diversification and superior performance compared to public markets as discussed earlier.

Several other factors contribute to this growing demand. Chief among them is the heightened volatility in public markets, often attributed to high-speed trading, global instability, and algorithm-driven institutional activity. Additionally, private placements provide access to uncorrelated or less correlated assets with major public market indices, offering a more resilient and insulated investment strategy.

In response to these dynamics, Registered Investment Advisors are turning to private placements to differentiate their practices and meet the evolving needs of their clients. For further insights, see our guide on Why Invest in Alternative Investments.

Why Wealth Managers are Embracing Private Placements

The growing shift toward private placements is gaining momentum among RIAs, financial advisors, and investment professionals, whether they are new to private investing or are already established in the space. Several factors, such as public market volatility and the diversification and performance advantages that private placements offer, are driving this momentum. As retail investors increasingly incorporate private placements into their portfolios, wealth managers are adapting to meet this demand — though some challenges remain.

Concerns for RIAs

Historically, wealth managers have been reluctant to consider private placements for a variety of reasons:

- Difficulty in reporting performance within client account statements

- Loss of wealth management fees due to reduced assets under management

- Limited resources or experience in conducting comprehensive due diligence

Solutions

Carofin and its affiliates have developed a unique private finance/private investment business that effectively addresses most concerns within the wealth management community. To support high-net-worth investors participating in syndicated private placements, particularly those using special purpose vehicles (“SPV”), Carofin, through CFG Financial Services, plays several key roles throughout the investment lifecycle:

- Fund Management: Carofin oversees day-to-day monitoring and takes actions required to support the underlying investment.

- Fund Administration: The firm maintains timely and accurate financial records, both at the fund level and for each investor, for all activity associated with a given SPV.

- Data Aggregation and Reporting: Carofin provides detailed individual account reports and consolidates them into portfolio statements. For wealth managers using Black Diamond, Carofin integrates investment data into the system, allowing private placements to be reported alongside traditional investments.

- Custodial Agent: Historically, Carofin maintained separate bank accounts for each investment and handled all fund flows between the SPVs and investors. Moving forward, Carofin expects Inspira (formerly Millenium Trust) to assume custodial responsibilities, ensuring that assets held in private placements continue to count toward AUMs for RIAs.

- Due Diligence Expertise: Carofin’s investment bankers and analysts have examined thousands of companies, and investors have placed over $1.1 billion in debt and equity investments across more than 200 offerings. The firm’s rigorous process includes gathering and analyzing comprehensive data on companies, management teams, financials, and internal financial controls. Wealth managers lacking resources can access this information easily through Carofin’s portal and decide whether to introduce clients to these carefully selected offerings. For more details, consult Carofin’s Due Diligence Checklist.

Financial Advisor Concerns

FAs also face obstacles when considering private placements for their clients. Common concerns include illiquidity, which is inherent in private investing, as well as high fees, their complexity (read: difficult to explain them to investors), and the significant due diligence required.

Solutions

Carofin addresses these concerns directly:

- Fees: No fees are assessed on clients or their financial advisors; the issuing companies compensate Carofin for its investment banking and syndication services.

- Educational Resources: To help advisors and their clients become more comfortable with private investing, Carofin offers a comprehensive Knowledge Base. This resource covers topics such as investment structures, risks, potential benefits, and key considerations before investing and is accessible through Carofin’s secure portal.

- Investment Minimums: Low investment minimums, typically set at $20,000-$25,000, encourage investors to diversify their private portfolios.

- Due diligence: Each investment is presented with a detailed summary of Carofin’s comprehensive due diligence, providing transparency and insight into the investment opportunity. FAs and their clients can review this material and participate in management calls with issuers to gain further clarity. Carofin’s staff is also available to address questions that arise during the decision-making process.

For three decades, Carofin and its affiliate have been dedicated proponents of private investing. As an investment bank and broker-dealer, Carofin structures both equity and debt investment opportunities, offering comprehensive support to RIAs throughout the entire investment lifecycle. Our platform simplifies portfolio diversification, offering low minimum investments and a straightforward onboarding process.

Carofin assists financial advisors and RIAs by conducting thorough issuer due diligence on each issuer. With a robust infrastructure, we enable RIAs to track client investment performance, provide transparent reporting, ensure streamlined regulatory compliance, and offer access to a comprehensive education center and online investor portals.

Discover how Carofin can support your RIA here.

- See Morgan Stanley, Public to Private Equity in the United States: A Long-Term Look. The proportion may surprise: approximately 70 percent of new capital in 2019 was raised privately; in 2017, $3.0 trillion of private capital was raised vs. $1.5 trillion in public markets.

- Center for Research in Security Prices; According to the Bureau of Economic Analysis, the number of listed companies as of Q1 of 2023 was 4,572, a drop of 43% since 1996.

- See Hamilton Lane Data via Cobalt, Bloomberg (January 2023).

- iCapital, 2023 iCapital Financial Advisor Survey: Alternative Investments Closer to Core

- Bain & Company, “Global Private Equity Report 2023”

Featured image by Tim Mossholder: https://www.pexels.com/photo/black-and-white-wooden-sign-behind-white-concrete-3690735/